Markets

US stocks face tests from Fed decision, tech-led earnings deluge

A wobbly US stock market will take its cues in the coming week from a Federal Reserve meeting set to shed light on the path for i...

Gulf-times.com

Live S&P 500, Nasdaq, and Dow Jones market news — market movers, sector performance, and Wall Street analysis. Updated daily.

· 23 articles

A wobbly US stock market will take its cues in the coming week from a Federal Reserve meeting set to shed light on the path for i...

Investors await the Federal Reserve's interest rate decision and corporate earnings reports. Technology giants and artificial intelligence companies will release their quarterly results. Rising oil prices and inflation concerns add complexity to the economi…

Up 0.46% to 51,947, the Dow Jones Industrial Average (DJINDICES:^DJI) recovered a portion of its Thursday loss, while the S&P 500 (SNPINDEX:^GSPC) edged up 0.05% to 7,412 and the Nasdaq Composite (NASDAQINDEX:^IXIC) slipped 0.64% to 24,976 on continued tech w…

U.S. markets closed mixed as the Nasdaq declined on chip stock weakness driven by concerns over heavy AI spending, while the Dow rose and the S&P 500 was nearly flat. Falling oil prices offered support, though geopolitical tensions and tariff developments kep…

Three indices dominate US equity market coverage. The S&P 500 — maintained by S&P Global — tracks 500 large-cap US companies selected by a committee based on market capitalization, liquidity, and sector representation. It is market-cap weighted, meaning larger companies like Apple, Microsoft, and NVIDIA have an outsized influence. As of 2025, the top 10 holdings represent approximately 35% of the index weight. The S&P 500 is the benchmark used by the majority of institutional investors, pension funds, and index funds globally.

The Nasdaq Composite lists over 3,000 stocks exclusively traded on the Nasdaq exchange and is heavily weighted toward technology and growth companies. The Nasdaq-100 (QQQ) tracks the 100 largest non-financial Nasdaq stocks and is even more tech-concentrated. The Nasdaq tends to outperform during low-rate growth environments and underperform during rate-hiking cycles (as seen in 2022, when it fell 33%).

The Dow Jones Industrial Average is the oldest US stock index (1896) and tracks 30 large US companies. It is price-weighted — a higher share price has more influence — making it less representative than the market-cap-weighted S&P 500. Despite its limitations, the Dow remains widely quoted in media as a barometer of US market sentiment.

| Sector | Approx. Weight | Key Companies | Characteristics |

|---|---|---|---|

| Information Technology | ~31% | AAPL, MSFT, NVDA | Growth, high P/E, rate-sensitive |

| Financials | ~13% | JPM, BAC, BRK.B | Benefits from higher rates, cyclical |

| Health Care | ~12% | UNH, JNJ, LLY | Defensive, growth from demographics |

| Consumer Discretionary | ~10% | AMZN, TSLA, MCD | Cyclical, consumer spending sensitive |

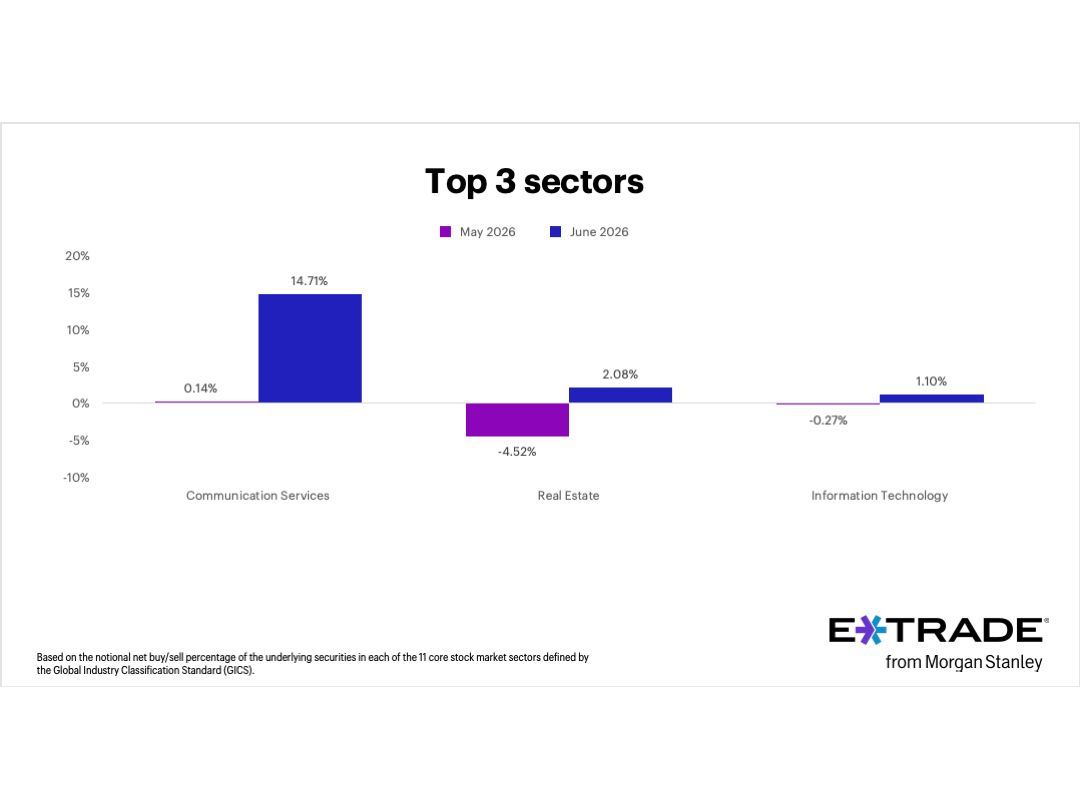

| Communication Services | ~9% | GOOGL, META, NFLX | Ad-revenue dependent, digital economy |

| Industrials | ~8% | CAT, HON, UNP | GDP-linked, capital expenditure cycle |

| Consumer Staples | ~6% | PG, KO, WMT | Defensive, dividend yield focus |

| Energy | ~4% | XOM, CVX, COP | Oil price driven, high dividend yield |

| Utilities | ~3% | NEE, DUK, SO | Defensive, rate-sensitive, dividend |

| Real Estate | ~2% | PLD, AMT, SPG | REIT structure, rate-sensitive |

| Materials | ~2% | LIN, APD, FCX | Commodity-linked, inflation hedge |

Approximate weights as of 2025. S&P Global rebalances quarterly. Source: S&P Global GICS, BlackRock sector data.

Understanding what moves the stock market requires tracking a small set of macro indicators that institutional investors watch most closely. The Federal Reserve's fed funds rate is the single most impactful variable — it determines the discount rate applied to future corporate earnings and the relative attractiveness of equities versus bonds. The 2022 bear market (-25% for S&P 500, -33% for Nasdaq) was almost entirely driven by the Fed raising rates from 0% to 5.25% in 12 months, the fastest tightening cycle since the 1980s.

The Consumer Price Index (CPI), released monthly by the Bureau of Labor Statistics, is the most market-moving economic data release after FOMC meetings. Core PCE (Personal Consumption Expenditures price index, excluding food and energy) is the Fed's preferred inflation measure. When CPI or PCE comes in above expectations, markets typically sell off as traders price in more Fed rate hikes. (Source: Bureau of Labor Statistics, Federal Reserve.)

The earnings season (four times per year) is the second major driver. The S&P 500 is ultimately priced off aggregate corporate earnings — the index has historically tracked earnings growth over long periods. In bull markets, P/E multiple expansion amplifies earnings growth; in bear markets, multiple compression can overwhelm even strong earnings.

| Period / Event | S&P 500 Move | Duration | Primary Cause |

|---|---|---|---|

| 2000–2002 Dot-Com Bust | -49% | 30 months | Tech bubble collapse, 9/11 |

| 2003–2007 Bull Market | +101% | 60 months | Credit expansion, housing boom |

| 2008–2009 Financial Crisis | -57% | 17 months | Lehman, CDO collapse, credit crisis |

| 2009–2020 Bull Market | +530% | 131 months (longest ever) | ZIRP, QE, earnings growth |

| Mar 2020 COVID Crash | -34% | 1 month (fastest -30% ever) | Pandemic lockdowns |

| Apr 2020–Dec 2021 | +114% | 21 months | Fiscal/monetary stimulus, vaccine |

| 2022 Bear Market | -25% | 12 months | Fed rate hike cycle 0→5.25% |

| 2023–2024 Bull Market | +53% | 24 months | AI boom, soft landing, rate cuts |

Historical data. Past performance does not predict future returns. Source: S&P Global, FactSet, Federal Reserve history.

Market Cap

Total market value of a company's outstanding shares. Large-cap: >$10B. Mid-cap: $2B–$10B. Small-cap: <$2B. Mega-cap: >$200B (Apple, Microsoft, NVIDIA).

P/E Ratio (Price-to-Earnings)

Stock price divided by earnings per share. The most basic valuation metric. S&P 500 forward P/E historically averages ~15x; currently elevated at ~21x driven by tech.

Bull / Bear Market

Bull market: +20% from recent low, sustained. Bear market: -20% from recent high. Correction: -10% to -20% decline. Historically, bull markets are longer and larger than bear markets.

Market Cap Weighting

Index construction method where larger companies have proportionally more influence. Used by S&P 500. Apple alone represents ~7% of the S&P 500.

VIX (Fear Index)

CBOE Volatility Index — measures expected 30-day S&P 500 volatility derived from options pricing. VIX <15: complacent. 15-25: normal. >30: elevated fear. >40: crisis-level.

Dividend Yield

Annual dividend per share divided by stock price. S&P 500 average yield ~1.3% (2025). High-yield sectors: Utilities, Staples, REITs. Growth sectors (Tech): typically 0% or minimal.

Short Selling

Borrowing and selling shares you don't own, hoping to buy them back cheaper. Profits from price declines. Short interest (% of float sold short) is a contrarian indicator when very high.

Market Breadth

Measure of how many stocks are participating in a market move. Strong breadth (most stocks advancing) signals a healthy rally. Narrow breadth (only a few mega-caps rising) signals fragility.

Stock market news on Vextor Capital is aggregated from third-party publishers. Vextor Capital is not the original publisher and is not responsible for content accuracy. Historical market data is sourced from S&P Global, FactSet, and Federal Reserve public databases.

Investment Disclaimer: Stock markets involve significant risk of loss. The S&P 500 has experienced multiple 20-50%+ drawdowns historically. Past performance — including long-run average returns of approximately 10% annually — does not guarantee future results. Individual stocks can fall to zero. Diversification reduces but does not eliminate risk. This content is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Consult a registered investment advisor (RIA) or broker-dealer before making investment decisions. (Source: SEC.gov investor education; FINRA investor alerts.)